Opportunities to integrate environmental drivers into mainstream risk assessments

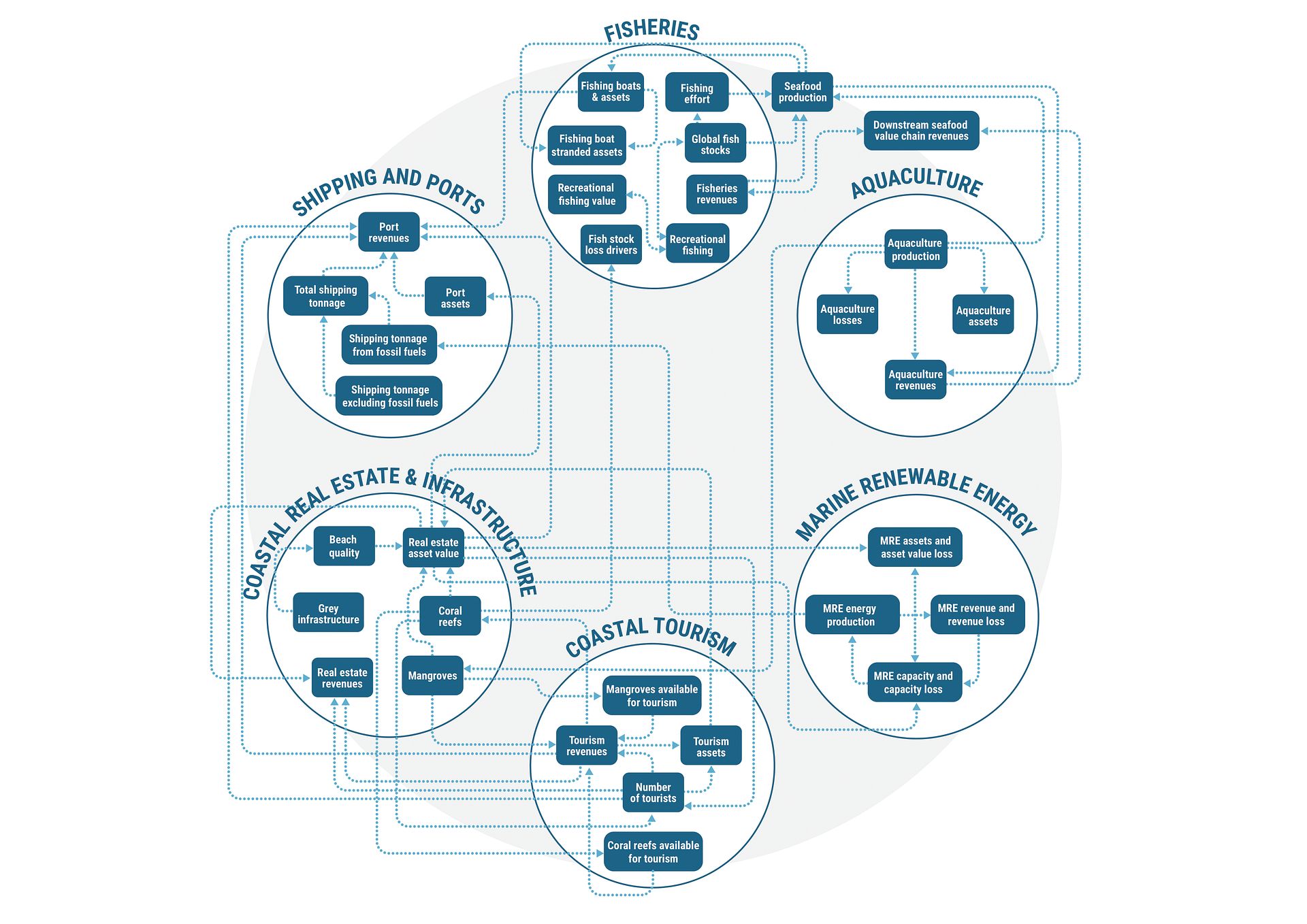

The system dynamics model allowed us to simulate feedback loops, tipping points, and tradeoffs in the blue economy, which are not captured in conventional risk valuation. For example, damaging fishing and aquaculture practices are detrimental to coral reefs and mangroves, which provide critical habitats for marine life and attract tourists. Decreased interest in tourism may lead to lost tourism revenue and slower appreciation of coastal property values. Therefore, understanding the interactions between commercial fisheries, coastal tourism, and coastal real estate is crucial in accounting for, and mitigating, the financial risks in these sectors.

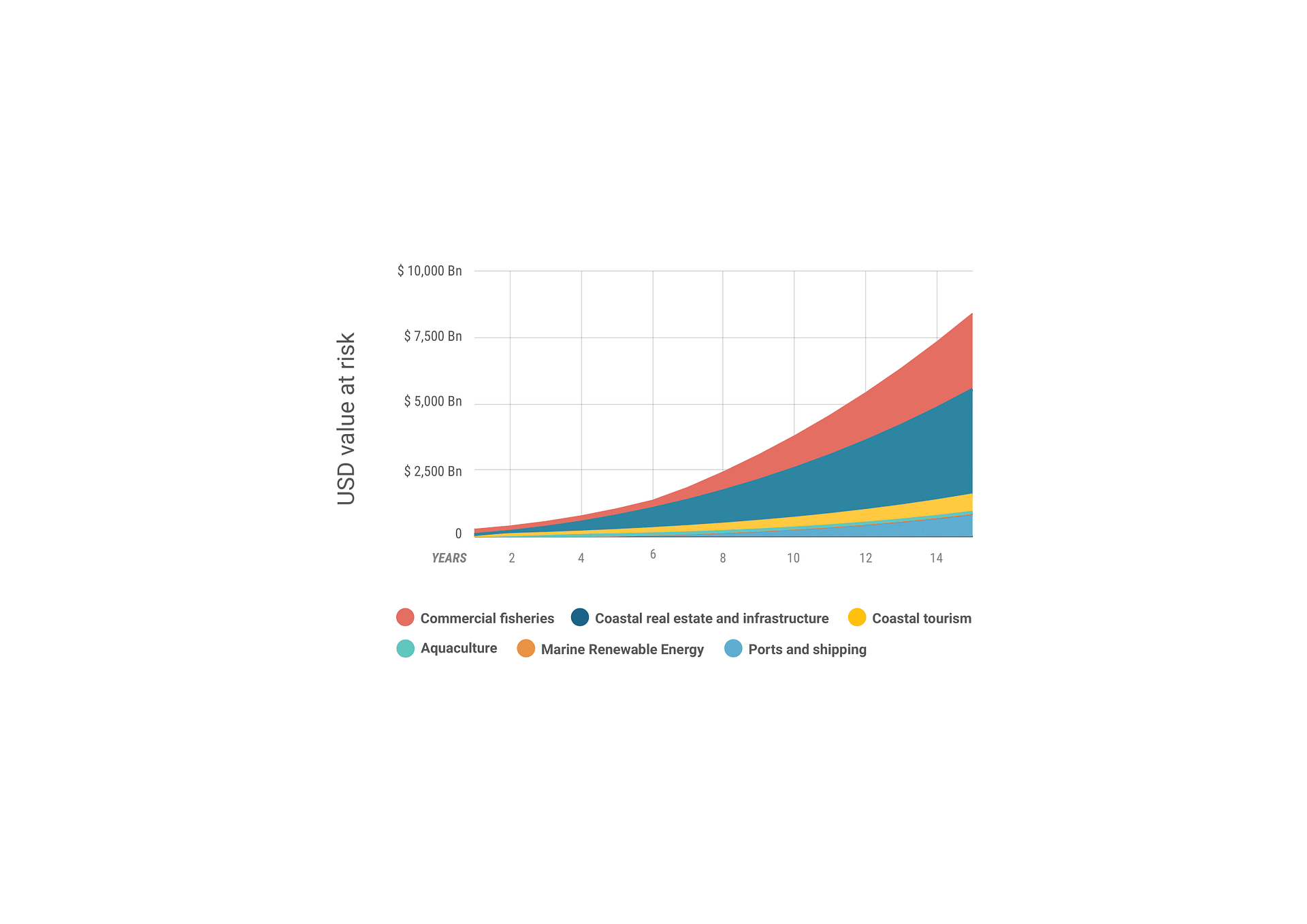

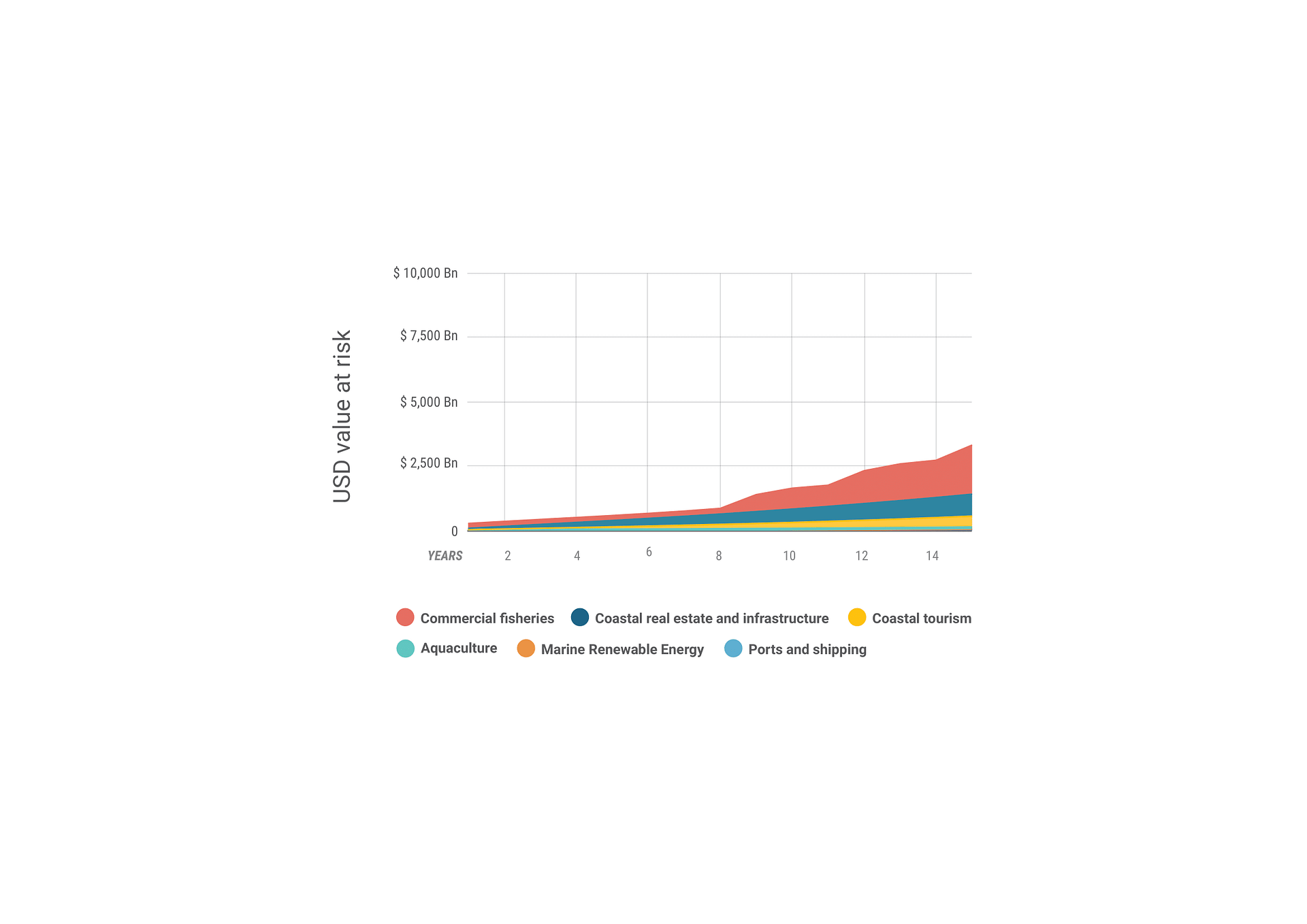

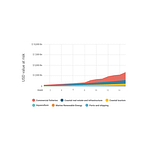

We found that up to two-thirds of publicly listed companies are, to some degree, dependent on a healthy ocean. There is significant VaR in a business-as-usual trajectory for the blue economy. Our global model estimates $8.4 trillion worth of assets and revenues are at risk in the next 15 years, and these risks are increasing exponentially. By adopting a more sustainable pathway, more than $5 trillion could be saved, according to our model.

This model can serve as a scenario-building and engagement tool for asset and portfolio managers to identify where exposure within an unsustainably managed blue economy may arise, and to see the effects of different interventions. While the methodology is designed for equities investors, the model is relevant for a wide range of financial services industries, including insurance, reinsurance, fund managers, those with sovereign debt, and asset managers.